Note: This is a very slightly modified version of a LinkedIn post I wrote in January 2026. The original post can be found here.

TL;DR:

While low-income (B40) home ownership did marginally surpass middle-income (M40) home ownership in 2024, the gap is relatively small (0.4 percentage points). The statement that M40 home ownership dropped is also incorrect, it actually increased. At the state level, M40 home ownership is still higher than B40 (except for Perlis, Sabah, and Sarawak). The official data and Rehda Institute’s statement (in this news article) does not establish a causal link to cross-subsidisation. Using this headline statistic (i.e., 0.4 p.p. higher) as proof of policy failure is premature, at best.

Nevertheless, the call to understand housing as an ecosystem rather than viewing housing narrowly in terms of affordability is commendable. To improve our understanding, we should among others, look at housing stocks versus flows, consider place-based policies, strengthen data quality and data literacy, and study the effects of home ownership on economic opportunity.

Reality check: Did home ownership among Malaysia’s middle-income (M40) group really fall below the low-income (B40) group as reported this week?

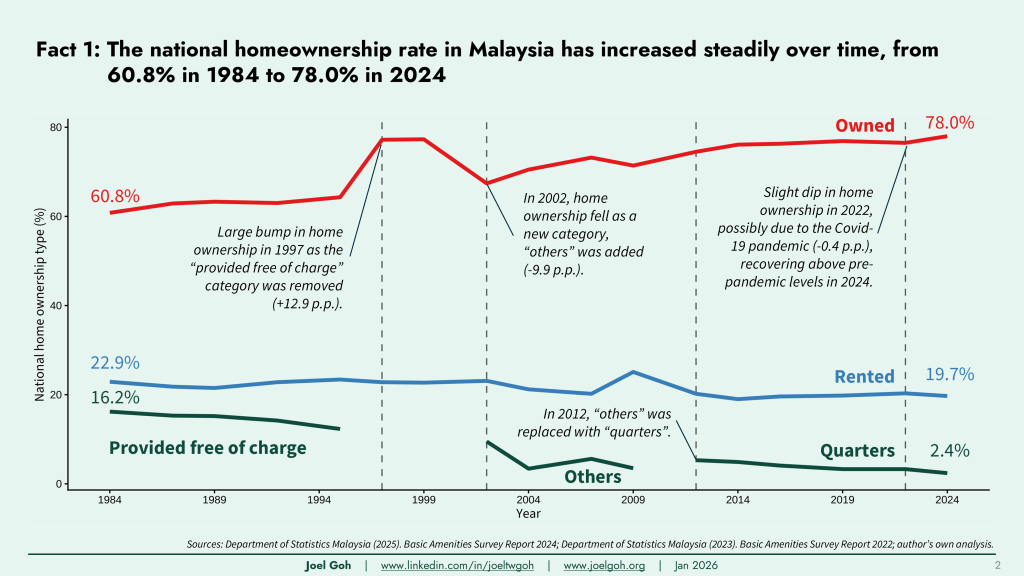

I pulled official DOSM data and did some quick-and-dirty pro bono analysis to sanity check Rehda Institute’s claim. See the facts in the images below. The majority of time was spent formatting and tweaking the charts (and then redoing them and adding more stuff). But there comes a point when one has to say “enough”. Feedback most welcome!

Conclusion: Rehda Institute’s statement that cross-subsidisation in the property industry has led to a drop in home ownership is yet to be proven.

Here are some further thoughts:

Limitations of this analysis: This quick and dirty analysis was done pro bono, but it already reveals how much more there is to issues of home ownership, even when working with the limited open data available today.

Statistical significance and uncertainty: The difference between B40 and M40 home ownership is relatively small (0.4 p.p.) With survey data and especially with 35% fewer respondents in 2024, that difference may be within the margin of error (we can’t be certain as DOSM’s data does not provide sufficient detail).

Stocks versus flows: Home ownership rate is a stock measure (a snapshot in time) rather than a measure of flow (houses bought in a specified period). A higher or lower home ownership rate does not reveal what is happening to first-time buyers, new launches, approvals, or affordability levels.

Income groups are not fixed: Membership in B40, M40, and T20 income groups shifts over time. Households can form and dissolve while members and structures of households also can change.

Lack of evidence from RehdaInstitute: While cross-subsidisation may be one of the factors leading to lower home ownership rates (especially for the middle-income group), robust analysis has yet to be presented and what is stated is mostly anecdotal. Other factors may have a stronger causal relationship.

Place-blind versus place-based policies: Comparing data for different states reveals that blanket place-blind policies may not be optimal for all – e.g., the housing dynamics of Kuala Lumpur are very different from Sarawak. Targeted place-based policies are more effective.

Better data and better data literacy: We clearly need better and more granular data. We also need better data literacy, even among “established experts” who have greater authority and therefore greater responsibility.

Home ownership limits economic opportunity: There is plenty of global research on how home ownership reduces geographical mobility and employment opportunities, especially among youth (e.g., Blanchflower and Oswald (2013)), but there is limited research on this in Malaysia (to the best of my knowledge).

Further research needed: Other possible home ownership research could include comparing income deciles (instead of B40, M40, T20), rural versus urban, age groups, longitudinal analysis, and more granular locations beyond the state-level. Additionally, the impact of housing quarters and potential of innovative financing and ownership/rental models should be explored.